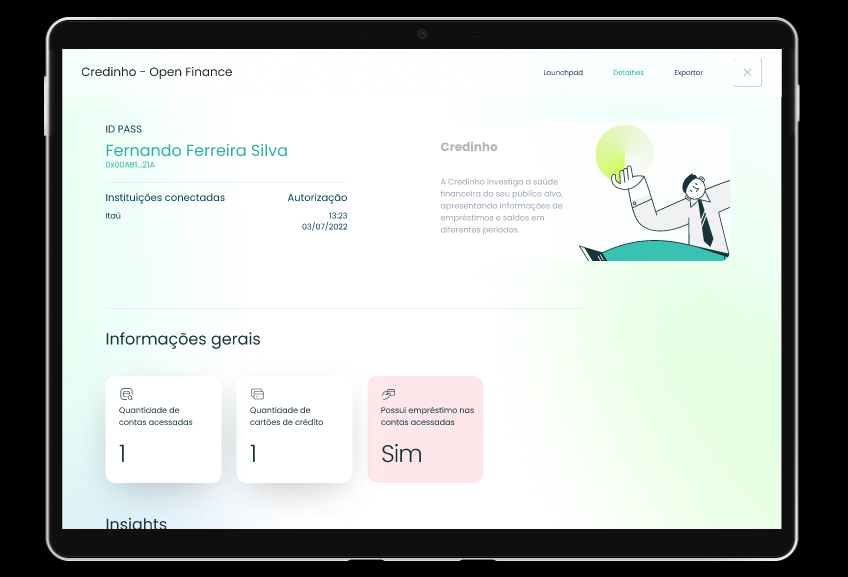

Use case: Open banking accounting

Humanizing credit for customer segmentation in a credit engine agnostic solution for a home equity ecosystem

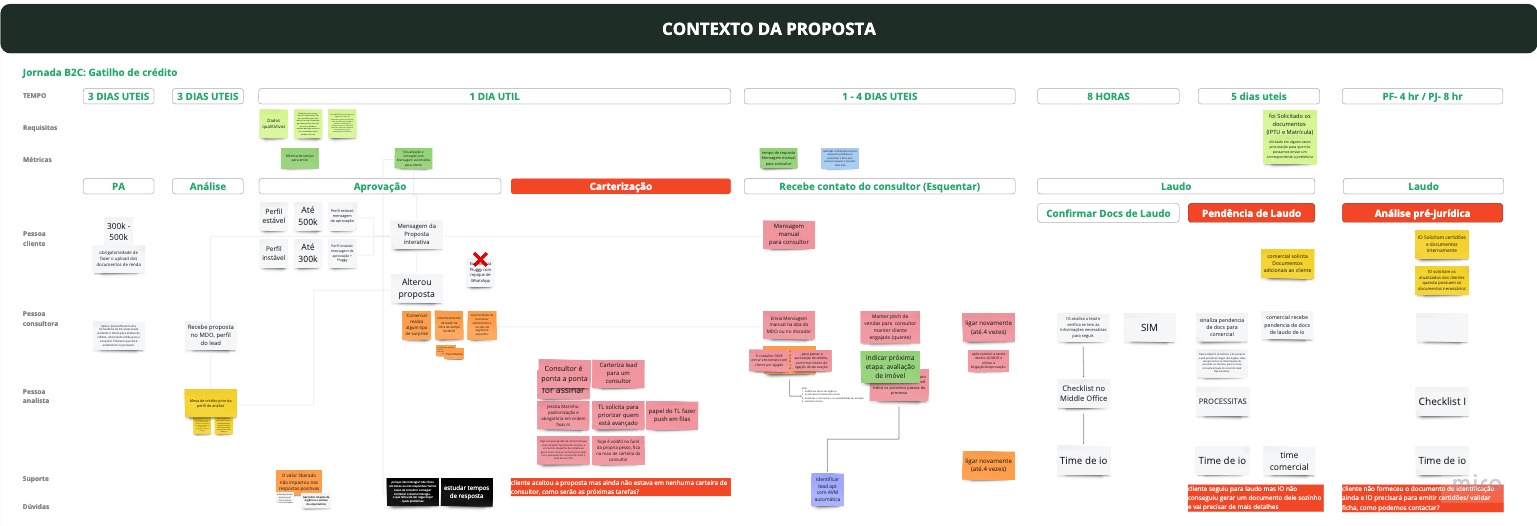

Context

The humanization of credit processes proved to be the safest way to measure the trust and credibility of customers in financial institutions, with a view to responding to Open Finance integration opportunities.

With this principle in mind, we worked on a digital transformation case study for the credit analysis area, where the main business problem was oriented towards the hypothesis of unifying the moment of communication of the sales executive, as an internal customer, by improving the self-service experience of the user of digital channels (end customer).

Problem

Instead of receiving several PDF files of bank statements, we seek to offer an internal and low-cost experience for the customer by qualifying the moment of contact with the final customer. The digital account integration solution aimed to minimize the need for manual income documents by offering account connection via open-banking in cycles of web scraping experiments.

In other words, we eliminate some issues involving business income offenders when we raise awareness of the verticals:

minimizing "income proof" properly as a major pain point for the customer;

the verification of unstable income information as operational (and manual) pain (from the credit analysis team and the commercial);

wear with communication in the customer experience (commercial and CRM);

mediation between "Trust vs. Risk" by the Corporate Business Intelligence areas.

Assumption: Sending multiple PDF files offers low end and internal customer experience

Hypothesis: Unify the moment of communication with the client to request income documents, offering connection to accounts via open-banking scraping

Solution

Optimized income tabulation, to be integrated via API, provided to the credit team in order to facilitate contact with the customer when obtaining the necessary documents for income tabulation.

Results

With this project, it was possible to:

Reduce origination CAC and increase the level of automation of the conveyor reflected in the E2E customer experience

Potentially offer a 49.9% reduction in the time from application to credit approval (with credit desk analysts)

150+ Pre-built credit statements for building predictive credit models (with data science engineers);

25% increase in risk score approval and termination rates (with portfolio team); 200 accounts connected in 2 weeks of experimentation (with the product, design and technology teams);

Insights

New customer segments as promoters of Open Banking

PF showed more confidence than PJ

Digital ageism against all odds and unlike stereotypes

Learning

Data Driven sampling with the commercial, Business Process and Product Hacking team

Experiments to understand customer perception for certain financial behavior profiles

Quali and Quanti triangulated data patterns helped to identify and promote correlations to new commercial segments in the context of real estate lending.

Friction:

In the first two occurrences of the experiment, there was no public engagement and with the data obtained it was not possible to contribute and support evidence or conclusions. The high level of uncertainty was positively influenced by this bias, as we knew how much we didn't know about something. However, we promote cycles of experimentation with potential learning.

Action:

To convert this, we started exploratory experiments (Wizard of Oz) to reduce harmful uncertainties and identify the true potential to be worked on (building a roadmap for the future Open Finance integration). With the experiment, it was possible to readjust the target audience - starting with individual clients, we found more opportunities for corporate clients given the representativeness of the executed data - influencing a high flow of interactions during the test cycle because the possible impact generated by the high volume of PJ customers being captured in the experiment. As a result, it was possible to have an even greater reach of market share for the B2B2C audience, in addition to important new skills for the technology team to develop, considering batch executions.

Lessons learned:

The open finance validation use cases needed to be tested with the 60+ public, which represented the largest volume of customers in this business unit, but also a new customer segment as a promoter of Open Banking. Thus, in 3 months we evidenced key opportunities in our partners' ecosystem with data that represented the familiarity and interest in the studied technology, in addition to demonstrating greater confidence in the brand by the user/customer.

Fully responsive

Modify website to fit various sizes of devices and enhance their responsiveness.

Pre-built layouts

Jumpstart your project with pre-built layouts such as headers, footers, and more.

Work with real content

Take advantage of CMS collections and integrate them with any design layout.

Outcomes

Prebuilt credit statements

for building the credit model

reduction in time from application to credit approval

increase in pass rates

and risk score termination

Conected accounts

in 2 weeks of experiment

Stakeholders mapping

The project focuses on the digital experience and innovation in credit using Design approaches in collaboration with partner teams from Product Hacking, Commercial, Marketing, ProdTech, Business Process, Credit Risk, Credit Platform Teams and others.

The contribution of Design time is oriented to the rearrangement of the area's processes, in the demands of each of the Content Design, Product Design and Service Design specialties.

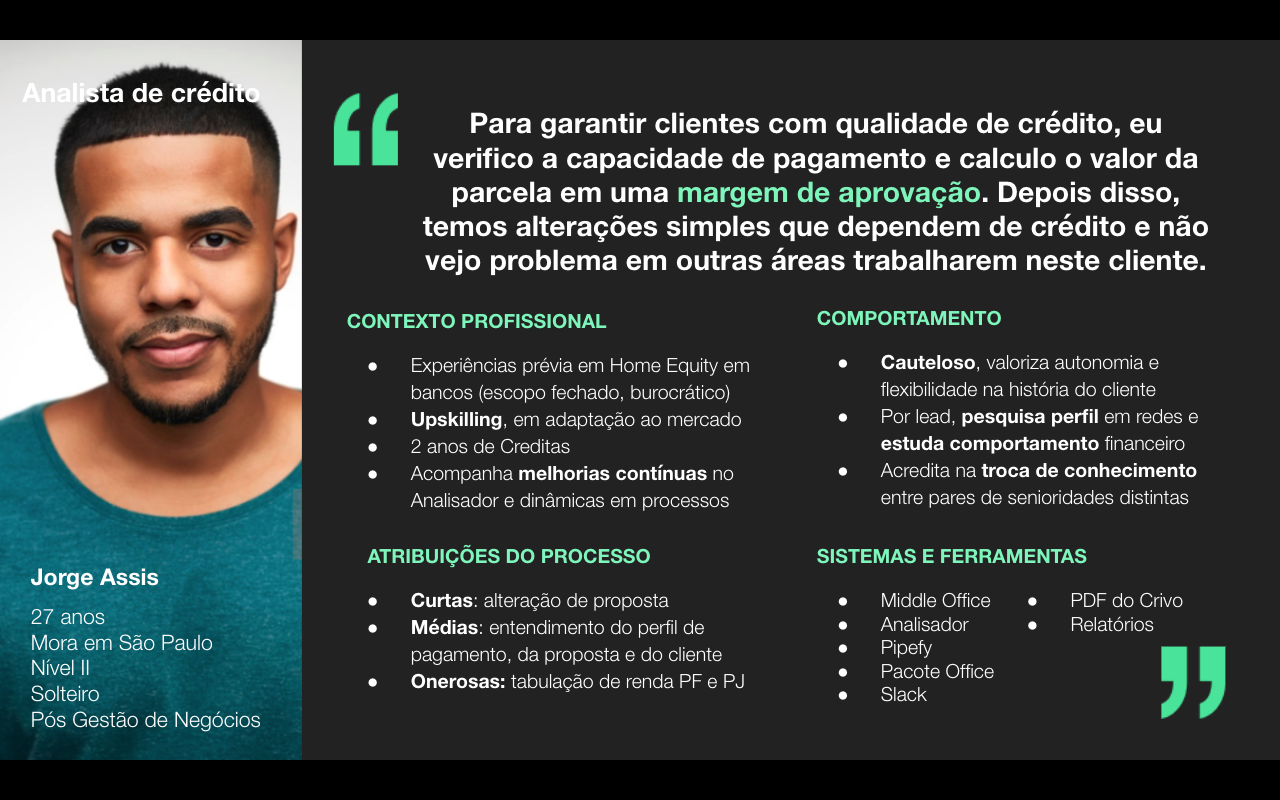

Main responsabilities

As a service designer my main responsabilities was:

1. Organization and monitoring of Design demands

2. Shared governance with the responsible teams

a. Monitoring the backlog and progress of the project

b. Follow-up internal journals and synchronized with the supplier

3. Integration of UX project strategies in the credit area

1.Identify gaps and integrate issues that contribute to the experience

A. Articulation and stakeholders management;

B. Follow-up process management and design prototypes to test implementation;

C. Co-creation of diagnostic report and design presentation for partners;

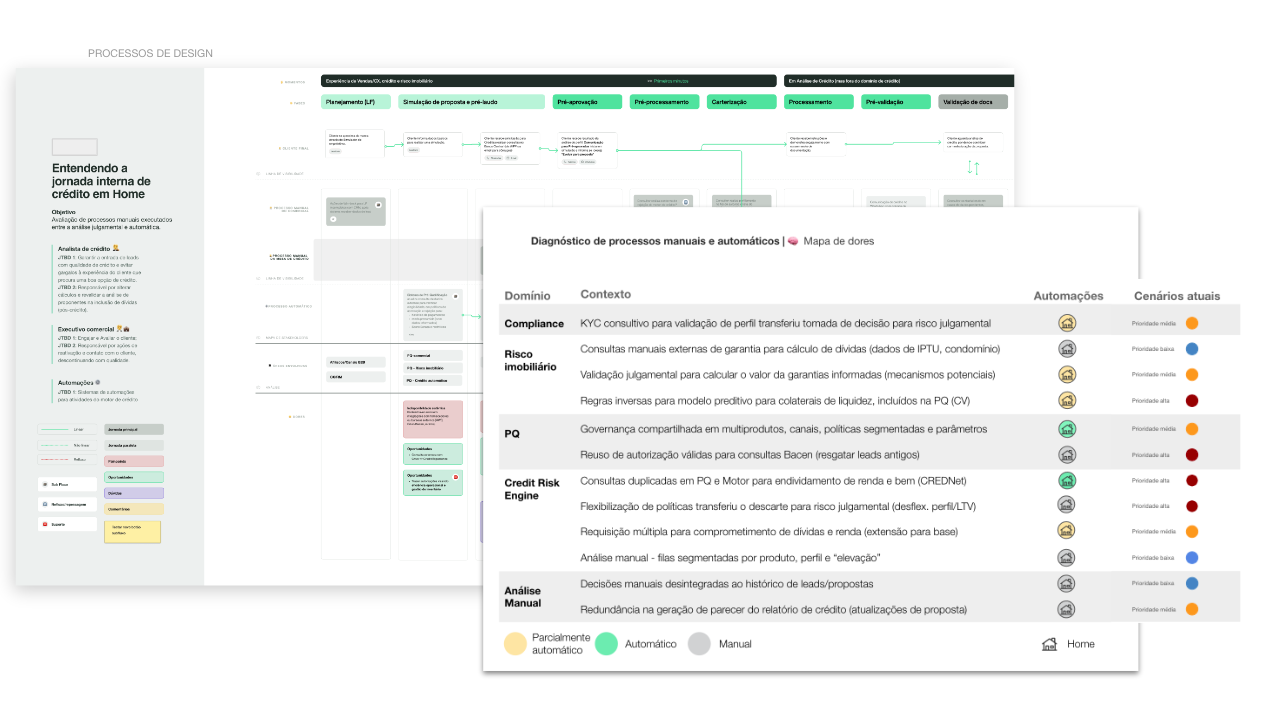

Engine vs Manual E2E diagnosis

Add animation to your designs to give them a more captivating look.

2. Explore different methodological approaches to resource and constraint analysis

A. Formulating criteria and specifications to aid estimation by the product team;

B. Support with tools for defining and validating hypotheses (in a simple and effective process that can guarantee the potential idea and its learning cycle);

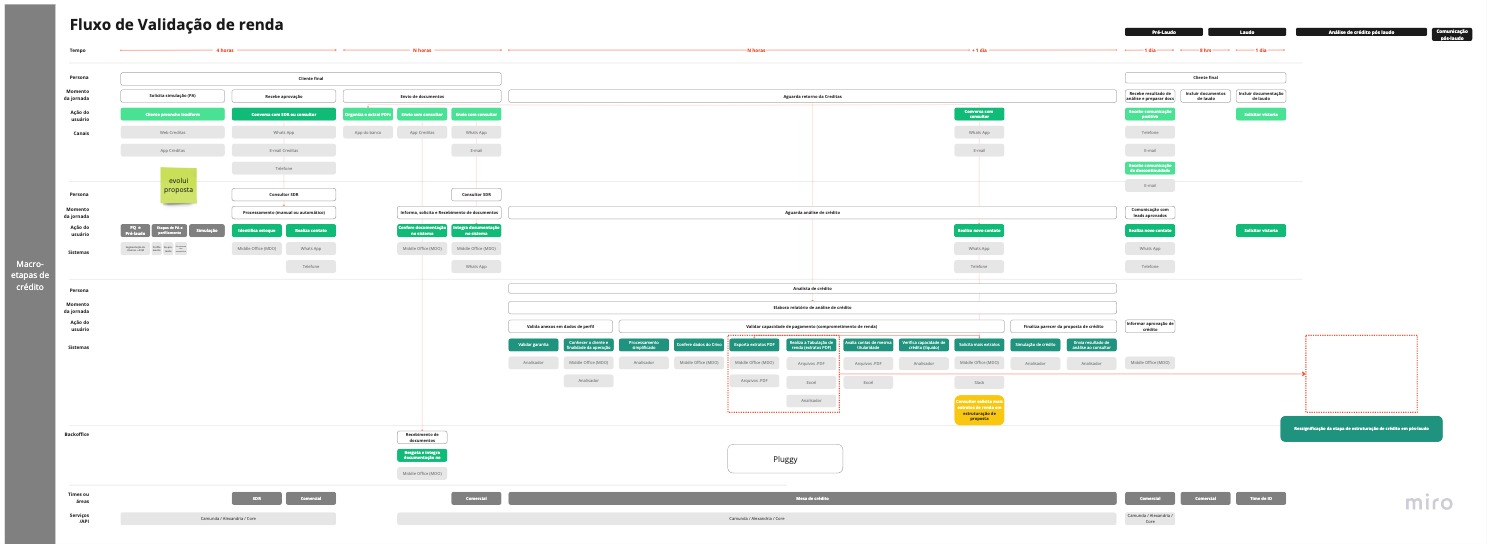

Internal User Journey issues

Establish consistent styles for elements throughout your project.

Business Process gaps

Save group of elements as components and reuse them.

Design audit previous LP Xp

Lead receives an automatic message via WhatsApp with access to a Landing Page

3. Identify decoupled and coupled service touchpoints to the platform

A. Monitoring the impact generated throughout the test (3 months of testing);

B. Planning and conducting surveys and tests with stakeholders and end users;

C. Deployment discovery (this would be prior to Test completion)

Randall Mercer

Head of Financing Operations

Randall Mercer

Head of Financing Operations Greta Lane

Business Process Coordinator

Greta Lane

Business Process Coordinator Camren Matthews

Engineer Specialist

Camren Matthews

Engineer Specialist Karina Sherman

Credit Team Coordinator

Karina Sherman

Credit Team Coordinator Leland Sanford

Product Manager

Leland Sanford

Product Manager Jacey Nielsen

Product Hacking Manager

Jacey Nielsen

Product Hacking Manager Ruth Collier

Commercial Coordinator

Ruth Collier

Commercial Coordinator Elianna Dalton

Content Designer

Elianna Dalton

Content Designer Parker Wolfe

Product Designer

Parker Wolfe

Product Designer Julio Hart

Service Designer

Julio Hart

Service DesignerSed ut perspiciatis unde omnis iste natus error sit voluptatem accusantium doloremque laudantium, totam rem aperiam, eaque ipsa quae ab illo inventore veritatis et quasi.